Key Insurance Terms Explained: 4 Essential Words That Make Pricing Clear (Premium, Deductible, Limit, Exclusion)

Insurance terms can feel like a different language. But once you understand four core words—premium, deductible, coverage limit, and exclusion—insurance pricing becomes much easier to interpret.

In this beginner-friendly guide from Insurance & Finance Education (operated by Kehost Team), you’ll learn what these terms mean, why insurers use them, how pricing factors shape premiums, and how choices like deductible impact and coverage limits affect your total insurance cost—without quotes, brands, or sales language.

1. A Simple Introduction Explaining the Topic in Plain Language

Insurance is designed to reduce financial shock. Instead of paying the full cost of a large, unexpected event alone (like a crash, theft, fire, storm damage, or a major medical bill), you pay a smaller, predictable amount to keep a policy active. If a covered event happens, the insurer may help pay according to the policy rules.

The confusion usually starts because insurance is built on definitions. A policy can look “cheap” until you notice a high deductible. Another policy can look “expensive” until you realize it has higher coverage limits and fewer exclusions. That’s why learning insurance terms matters: they explain how insurance cost is shared between you and the insurer.

As you read, keep this simple idea in mind:

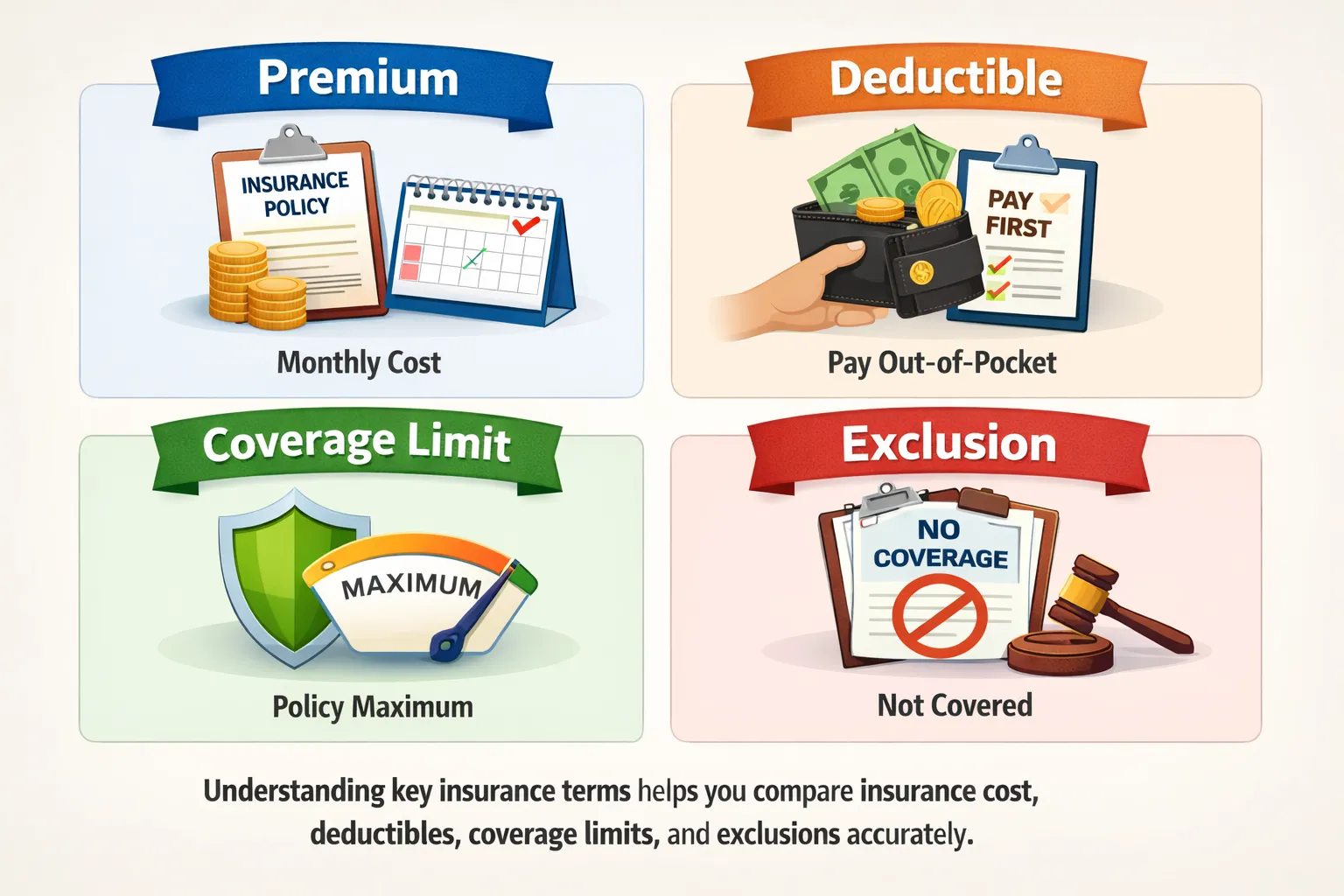

- Premium = what you pay to keep coverage active.

- Deductible = what you pay first (in parts of the policy where it applies) when a claim happens.

- Coverage limit = the maximum the policy may pay for certain types of losses.

- Exclusion = something the policy does not cover.

If you want a simple foundation before we go deeper into insurance terms, this internal guide can help:

How Insurance Works: Premiums, Risk Pooling & Claims.

3. Key Factors That Influence Insurance Costs (Age, Risk, Location, Coverage, Deductibles, etc.)

Pricing factors vary by country and insurance type, but globally insurers often evaluate similar categories. Think of these as inputs that shape your risk profile (how likely a claim is) and the expected claim cost (how expensive it may be).

Personal and risk profile factors

- Age and experience: Some age groups or experience levels can correlate with different claim patterns, depending on product type.

- Claims history: Prior claims can signal higher probability of future claims (details matter and rules vary).

- Behavior and usage patterns: More exposure can mean higher risk—for example, higher driving mileage for auto coverage.

- Health indicators (where relevant): For some products, health or lifestyle risk signals can affect pricing.

Location and environment factors

- Where you live or operate: Local accident rates, theft rates, fraud patterns, and claim frequency can influence insurance cost.

- Weather and natural hazards: Flood, storm, wildfire, or earthquake exposure can affect expected claim costs.

- Local service costs: Repair, labor, and medical costs can raise or lower expected payouts.

Coverage design factors

- Coverage type: Broader coverage usually increases premium because more situations are covered.

- Deductible impact: A higher deductible often lowers premium (you pay more first), while a lower deductible often raises premium.

- Coverage limits: Higher limits often increase premium because the maximum potential payout is higher.

- Exclusions and conditions: More restrictions can reduce premium, but they can also reduce real protection.

Most insurance pricing is the result of combining multiple pricing factors—not one single detail. Understanding these categories makes insurance terms feel less mysterious.

To see pricing factors in a real example, read:

Why Car Insurance Premiums Differ by Driver.

4. Why Insurance Premiums Vary From Person to Person

Insurance premiums vary because people are not identical in risk, exposure, or coverage design. Even when two people have “the same type of insurance,” they may not have the same deductible, the same coverage limits, or the same exclusions.

Premiums often differ due to:

- Different risk profiles: different exposure and risk signals (for example, history and usage patterns).

- Different expected claim costs: the same incident can cost more in one place than another (repairs, medical costs, legal processes).

- Different coverage choices: higher limits, broader coverage, and lower deductibles often increase premium.

- Different policy rules: exclusions, waiting periods, sub-limits, and conditions can change what is actually covered.

This is why comparing insurance cost requires comparing the full structure of the policy, not just the premium number.

5. General Cost Ranges Explained Carefully (Without Exact Prices)

Many beginners search for the “average cost” of insurance. The most accurate explanation is that it varies widely and depends on multiple factors. Insurance cost depends on your risk profile, location, coverage limits, deductible impact, and how broad the coverage is.

Instead of focusing on a single global number (which can be misleading), it helps to think in broad patterns:

- Often lower-cost situations: lower-risk profile signals, fewer claims, stable usage patterns, higher deductibles, moderate coverage limits, and narrower coverage.

- Often higher-cost situations: higher exposure to risk, prior claims, high hazard locations, expensive-to-repair assets, lower deductibles, higher coverage limits, and broader coverage.

Remember: “average” is just a broad statistic. Even within the same city, two people can pay very different premiums because their coverage choices and risk profile differ.

6. Premium vs Deductible vs Coverage Limit vs Exclusion (Simple Explanations)

This section explains the four most important insurance terms in plain language. Once these are clear, insurance pricing becomes much easier to understand.

Premium: the cost to keep coverage active

Your premium is what you pay to keep the policy in force. It’s predictable (monthly or yearly), and it exists whether you file a claim or not. Premium is part of your total insurance cost, but it is not the only cost you may face.

Deductible: what you pay first (where it applies)

A deductible is the amount you pay out of pocket before the insurer pays on a covered claim in the parts of the policy where deductibles apply. The deductible impact is important because it changes how costs are shared:

- Higher deductible: often lowers premium because you take on more of the first part of the loss.

- Lower deductible: often raises premium because the insurer may pay more often, including smaller claims.

Coverage limit: the maximum the policy may pay

Coverage limits set the maximum amount the insurer may pay for certain categories of loss. Limits can be per claim, per person, per incident, or over the policy period, depending on the product.

Exclusion: what the policy does not cover

An exclusion is a situation, type of loss, or condition that the policy does not cover. Exclusions exist to define boundaries of coverage and keep pricing manageable.

Simple check: If you understand these four insurance terms, you can read most policy summaries with much more confidence.

7. How Deductibles, Limits, and Coverage Choices Affect Total Cost

Many pricing surprises happen because people compare premiums without comparing the full policy structure. Two policies can have similar premiums but very different real protection because their deductibles, coverage limits, and exclusions differ.

Your total insurance cost is more than the premium

Think of total insurance cost as a combination of:

- What you pay regularly: premium

- What you may pay if something happens: deductible (where applicable)

- What you may pay if costs exceed limits: any amount above your coverage limits

- What you may pay because of exclusions: uncovered events or conditions

Why deductible impact can change pricing fast

A deductible is one of the quickest levers to change premium. If you choose a higher deductible, you often lower the premium because you are taking more of the first loss. If you choose a lower deductible, you often raise the premium because the insurer may pay more frequently.

Why coverage limits matter for both price and protection

Higher coverage limits usually increase premium because they increase the insurer’s maximum potential payout. Lower limits can reduce premium, but they can also increase your financial exposure in serious losses.

Why exclusions change the “real value” of a policy

Two policies can have the same premium, but one can exclude more scenarios. That can make a policy feel cheaper but less useful when a real-life event happens. Understanding exclusions is a core part of understanding insurance terms and insurance cost.

If you want a broader money-planning foundation that helps you choose deductibles and limits more confidently, read:

Financial Literacy: Why It Matters (Beginner Guide).

8. Common Misconceptions People Have About Insurance Pricing

Misconception 1: “The cheapest premium is always best.”

A lower premium can come with a higher deductible, lower coverage limits, or more exclusions. That may reduce real protection when you need it most.

Misconception 2: “If I pay a premium, everything is covered.”

Policies cover specific risks under specific conditions. Deductibles, exclusions, documentation requirements, and limits all affect how a claim works.

Misconception 3: “My premium should match my friend’s.”

Different risk profiles, locations, usage patterns, and coverage design can produce different premiums—even with similar situations.

Misconception 4: “Average cost tells me what I’ll pay.”

Average cost is a broad statistic. Your personal premium depends on pricing factors, your risk profile, and the coverage choices you select.

Misconception 5: “Insurance is wasted money if I don’t claim.”

Insurance is mainly protection against rare but expensive events. Not claiming can mean you avoided a major financial shock, which is often a good outcome.

9. Practical, Non-Sales Tips for Managing or Reducing Insurance Costs Safely

These tips are educational and focused on safety and clarity. The goal is to reduce avoidable risk and choose coverage intelligently, without cutting protection too far.

1) Compare policies “like for like”

When comparing insurance cost, match the same coverage types, deductible level, and coverage limits. Otherwise, you may compare two very different products.

2) Choose a deductible you can realistically pay

Higher deductibles can reduce premium, but only if you could pay the deductible without stress after an event. Deductible impact is important, but affordability matters more than the lowest premium.

3) Review coverage limits as a risk decision

Lower limits can reduce premium but may increase your exposure in severe incidents. Think in terms of “what would happen in a worst reasonable case?”

4) Learn the exclusions before relying on the policy

Exclusions define what the policy will not help with. Understanding them reduces surprises and helps you compare policies more fairly.

5) Reduce risk where you can

Many pricing factors relate to risk and exposure. Safe habits, sensible maintenance, secure storage, and reducing avoidable hazards can support a healthier risk profile over time.

6) Keep details accurate and updated

Changes in location, usage, and household details can affect pricing and coverage validity. Accurate information supports fair pricing and fewer claim disputes.

7) Build a small emergency buffer

Even a modest emergency fund can help you handle deductibles and uncovered costs without relying on high-cost debt.

For additional consumer education, you can explore:

Insurance Information Institute (III)

and

Consumer Financial Protection Bureau (CFPB).

10. Educational Disclaimer (Learning Only)

Educational disclaimer: This content is for general education only and is not insurance, legal, financial, or medical advice. Insurance rules, pricing factors, coverage limits, deductible impact, exclusions, and policy terms vary by country, provider, and product type. Always read your policy documents for your specific terms and conditions.

Conclusion

Insurance becomes much easier to understand when you know the core insurance terms. Your premium is what you pay to keep the policy active. Your deductible influences how costs are shared when a claim happens. Your coverage limits define the maximum the policy may pay, and exclusions define what is not covered. Together—along with your risk profile and other pricing factors—these elements explain why insurance cost varies widely from person to person.

When you read insurance documents with these concepts in mind, you can interpret pricing more clearly, compare options more fairly, and make decisions based on understanding rather than confusion.